Introduction

A business may have miscellaneous forms of

income, for example, from renting out property.

When a business entity has income from

sources where payments are made in advance or in arrears. The accruals basis of

accounting applies, and the amount of income to include in profit and loss for

a period is the amount of income that relates to that period. It may therefore

be necessary to apportion income on a time basis and there may be unearned

income or accrued income to account for.

Unearned income

This is where a business has received income

in advance. For example, a business might rent out a property for which the

tenant must pay in advance. Only the income that relates to the period is

recognised in the statement of comprehensive income and the balance is

recognised as a liability of the business. (Note that it is an asset of the

tenant).

The method of calculating income for the year when there

is unearned income is the same in principle as the method of calculating an

expense for the year when there is an accrued charge or a prepaid expense.

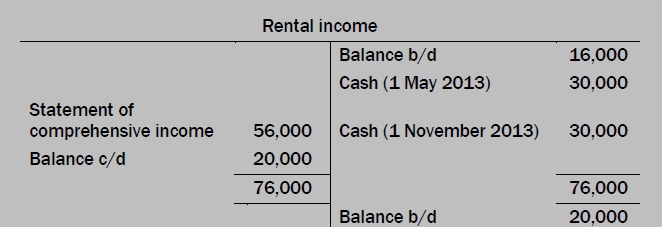

Example: Unearned income

A

business rents out a part of its premises.

The

rent is payable every six months, on 1 May and 1 November in advance.

The

company has a year end of 31 December.

The

annual rental for the year to 30 April 2013 was Rs. 48,000 (received in two

amount so of Rs.24,000 on 1 May 2012 and 1 November 2012).

The

annual rental and Rs. 60,000 for the year to 30 April 2014 (received in two

amount so of Rs.30,000 on 1 May 2013 and 1 November 2013).

Income

for the year ending 31 December 2013 is:

For

the 4 months 1 January – 30 April 2013:

4/12 ´ Rs. 48,000

16,000

For

the 8 months 1 May – 31 December 2013:

8/12 ´ Rs. 60,000

40,000

Rental income for the year to 31

December 2013 56,000

At

31 December 2012 there was unearned rental income for the period 1 January – 30

April 2013.

The

amount of unearned income is 4/12

of the Rs. 24,000 received on 1

November 2012 which came to Rs. 16,000. (This represents 4 months at Rs. 4,000

per month)

This

was included as a current liability in the statement of financial position as

at the end of the last financial year.

At

31 December 2013 there is unearned rental income for the period 1 January – 30

April 2014.

The

amount of unearned income is 4/12

of the Rs. 30,000 received on 1

November 2013 which comes to Rs. 20,000. (This represents 4 months at Rs. 5,000

per month)

This

is recognised as a current liability as at the end of the financial year.

Unearned income (just as for prepayments and accruals)

can be accounted for using either one or two accounts to record the transactions.

If two accounts are used the closing unearned income liability must be reversed

to the income account at the start of the next period (just as is the case for

prepayments and accruals).

Approaches for unearned income

- Method 1

- Method 2

Method 1: Two accounts method

Income has been paid to the business but some

of it relates to the next period.

This amount must be transferred from the

income account to a liability account

Example: Unearned income

Debit Credit

Income X

Unearned income (liability)

X

Example (continued): Unearned income

The double entry is

as follows:

|

| Unearned income |

Method 2: One account method

The unearned income is brought down as a

liability on the income account.

There are two ways of achieving this.

The total income for the period can be calculated and transferred

to the statement of comprehensive income (Dr Income account; Cr Statement of comprehensive

income) leaving a balancing figure on the expense account as the unearned

income liability; or

The unearned income liability can be calculated and recognised in

the expense account leaving the amount transferred to the statement of comprehensive

income (Dr Income account; Cr Statement of comprehensive income) as a balancing

figure

Example

(continued): Unearned income (One account approach)

The double entry is as follows:

|

| Unearned income |

Accrued income

This is where a business receives income in

arrears. For example, a business might rent out a property for which the tenant

must pay in arrears. The tenant might owe the business money at the business’s

year-end.

All of the income that relates to the period

must be recognised in the statement of comprehensive income. It is necessary to

recognise the amount owed to the business as an asset at the year-end.

The method of calculating income for the year when there

is accrued income is the same in principle as the method of calculating an

expense for the year when there is an accrued charge or a prepaid expense.

Example:

Accrued income

A

business rents out a part of its premises.

Rentals

are payable each quarter in arrears on 31 January, 30 April, 31 July and 31

October.

The

company has a year end of 31 December.

The

annual rental was Rs. 30,000 per year until 31 October 2013 (or Rs. 2,500 per

month received in 4 amounts of Rs.7,500 on 31 January, 30 April, 31 July and 31

October).

The

annual rental was increased to Rs. 36,000 per year from 1 November 2013 (or Rs.

3,000 per month received in 4 amounts of Rs.9,000 on 31 January, 30 April, 31

July and 31 October).

Income

for the year ending 31 December 2013 is:

Rs.

For

the 10 months 1 January – 31 October 2013:

10/12 ´ Rs. 30,000

25,000

For

the 2 months 1 November – 31 December 2013:

2/12 ´ Rs. 36,000

6,000

Rental

income for the year to 31 December 31,000

At

31 December 2012 there was rental earned but not yet received.

This

is the rental income for November and December 2012, which will not be received

until 31 January 2013.

The

amount of the accrued income is Rs. 5,000 (2/3

of 7,500 or 2 months at Rs.

2,500 per month) and was included in last year’s income and recognised as a

current asset at the end of last year financial year.

At

31 December 2013 there is rental earned but not yet received.

This

is the rental income for November and December 2013, which will not be received

until 31 January 2014.

The

amount of the accrued income is Rs. 6,000 (2/3

of 9,000 or 2 months at Rs.

3,000 per month) and is included in income and recognised as a current asset at

the end of the financial year.

Accrued income (just as for prepayments and accruals) can

be accounted for using either one or two accounts to record the transactions.

If two accounts are used the closing accrued income asset must be reversed to

the income account at the start of the next period (just as is the case for

prepayments and accruals).

Approaches for Accrued Income

- Method 1

- Method 2

Method 1: Two accounts method

Income has been earned in the current period.

This amount must be recognised.

Example: Accrued income

Debit Credit

Accrued income (asset) X

Income X

Example (continued): Accrued income

The double entry is

as follows:

|

| Accrued income |

Method 2: One account method

The accrued income is brought down as an

asset on the income account.

There are two ways of achieving this.

- The total income for the period can be calculated and transferred to the statement of comprehensive income (Dr Income account; Cr Statement of comprehensive income) leaving a balancing figure on the expense account as the accrued income asset; or

- The accrued income asset can be calculated and recognised in the expense account leaving the amount transferred to the statement of comprehensive income (Dr Income account; Cr Statement of comprehensive income) as a balancing figure

Read Also:ACCRUALS AND PREPAYMENTS INTRODUCED

Example (continued): Accrued income (One account approach)

The double entry is

as follows:

|

| Accrued income (One account approach) |

No comments:

Post a Comment