Depreciation is a method of spreading the cost of a non-current asset over its expected useful life (economic life), so that an appropriate portion of the cost is charged in each accounting period.

Definitions (from IAS 16)

Depreciation: The systematic allocation of the depreciable amount of an asset over its useful life.

Depreciable amount: The cost of an asset (or its revalued amount, in cases where a non-current asset is revalued during its life) less its residual value.

Residual value: The expected disposal value of the asset (after deducting disposal costs) at the end of its expected useful life.

Useful life: The period over which the asset is expected to be used by the business entity.

Example: Depreciation

An item of equipment cost Rs. 300,000 and has a residual value of Rs. 50,000 at the end of its expected useful life of four years.

Depreciation is a way of allocating the depreciable amount of Rs. 250,000 (= Rs. 300,000 - Rs. 50,000) over the four years of the asset’s expected life.

Depreciation should be charged as an expense in the statement of comprehensive income each year over the life of the asset.

Depreciation of a new asset commences from the date that an asset is available for use.

Most non-current assets must be depreciated, although there are some exceptions to this rule. For example, land is not depreciated because it has an indefinite useful life.

2. Accounting for depreciation

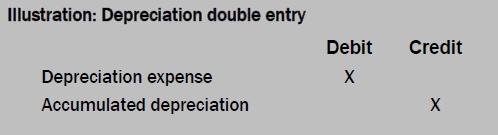

The double entry for depreciation is carried out using two accounts (for each category of non-current asset).

|

| Depreciation double entry |

The balance on the depreciation expense account is taken to the statement of comprehensive income as an expense for the period.

The accumulated depreciation account contains all of the depreciation recognised to date. When the final statement of financial position is prepared it is deducted from the cost of the assets. The non-current asset figure in the statement of financial position is made up of two figures, the cost less accumulated depreciation.

The balance on the accumulated depreciation account is carried forward as a (credit) balance at the end of the period and appears in the statement of financial position as a deduction from the cost of the non-current assets. The figure that appears in the statement of financial position is known as the carrying amount (or net book value).

|

| Carrying amount of anon-current asset |

Accounts in the ledger for non-current assets and accumulated depreciation

There are separate accounts in the general ledger for each category of noncurrent assets (for example, an account for land and buildings, an account for plant and machinery, an account for office equipment, an account for motor vehicles, and so on) and the accumulated depreciation for each of these categories of non-current assets.

This means that each category of non-current assets can be shown separately in the financial statements.

3. The purpose of depreciation

It is important to understand the purpose of depreciation. Depreciation is an application of the accruals concept or matching concept.

When a non-current asset is purchased the cost is:

· taken to the non-current asset account at cost and

· shown in the statement of financial position.

The cost is capitalised. However this asset is used within the business in order to earn profits. Therefore some element of its original cost must be charged to the statement of comprehensive income (‘charged to profit and loss’) each period in order to match the ‘consumption’ of the cost or value of the assets with the income that the asset is generating.

Depreciation is the element of the cost of the non-current asset that is charged to the statement of comprehensive income each period.

There are several ways of calculating the depreciation charge for the year.

Read Also: NON-CURRENT ASSETS

Disposal can occur at any time and need not be at the end of the asset’s expected useful life.

ReplyDeleteThe effect of a disposal on the statement of financial position (or accounting equation).Thanks for sharing useful Information with me and it's very helpful. Being Best CA coaching Centre in Hyderabad One of the Leading Coaching Centres in Hyderabad for Chartered Accountancy.

If the Total of Credit side is more than the Debit side, then the difference on the Debit Side will be represented as “Goodwill A/c.Thanks for sharing useful Information with me and it's very helpful. Being Best CA coaching Centre in bangalore One of the Leading Coaching Centres in bangalore for Chartered Accountancy.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteSparkEV is also the first EV from Chevy (aka, GM). You might claim EV1 was the first EV, but EV1 was never meant to be sold. If one goes by GM electric vehicle that's not sold to consumers, lunar rover from Apollo mission would be the first GM EV, or maybe there were EV prototypes before then. Obviously, we don't count those, so we shouldn't count EV1, either.Thanks for sharing useful Information. Being Best CA coaching Centre in Coimbatore One of the Leading Coaching Centres in Coimbatore for Chartered Accountancy.

ReplyDelete